With its cyclical nature, the energy sector experiences swings that mirror economic trends, with supply and demand constantly in flux. Right now, the natural gas (NGX24) space is making a comeback, fueled by rising demand and the urgent need for infrastructure. This landscape is shifting due to the rise of artificial intelligence (AI), which is driving explosive growth in data center energy needs. According to the International Energy Agency (IEA), global data center electricity consumption is set to double by 2026, placing natural gas in the spotlight.

At the core of this change are midstream energy companies - often the underappreciated contributors to the oil and gas industry. These firms handle the transportation and storage of natural gas, which allows them to enjoy more stable cash flows and consistent dividend payouts as the “landlords” of the industry.

Amid an unpredictable energy market, investing in high-yield dividend stocks with a steady base of earnings is one way to help buffer against volatility. Canada-based Pembina Pipeline Corporation (PBA) stands out as one solid pick that pays a nearly 5% dividend yield, and is recommended by Jefferies as a compelling alternative to its U.S. counterparts.

Let’s dive deeper into why this dividend-paying midstream energy stock could be a smart buy.

About Pembina Pipeline Stock

Calgary-headquartered Pembina Pipeline Corporation (PBA), incorporated in 1954, is a key player in North America's energy infrastructure. Its vertically integrated model spans the entire hydrocarbon value chain, providing energy transportation and midstream services to some of the continent's most productive basins. Dual-listed on the New York (NYSE) and Toronto stock exchanges (TSX), Pembina boasts significant capacity, handling 3 million barrels per day of hydrocarbon transportation and 6 billion cubic feet of gas processing daily.

With three business units - Pipelines, Facilities, and Marketing & New Ventures - Pembina offers diverse services, from conventional and oil sands pipelines to infrastructure for natural gas and NGLs like ethane and propane. Its marketing arm actively trades hydrocarbons across multiple North American basins, strengthening its foothold in the energy markets.

Plus, with 65% to 75% of its revenue secured through fee-based, take-or-pay contracts, Pembina enjoys steady income regardless of market volatility, making it a stable player in the energy sector.

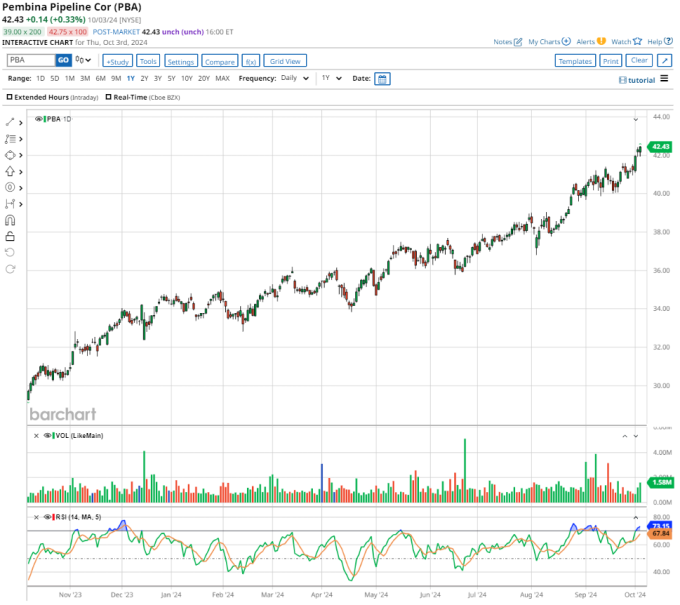

Shares of this midstream energy company have been on a solid upswing, climbing 49.4% over the past 52 weeks and rallying 19.5% in just over the past six months. That outpaces not just S&P 500 Energy Sector SPDR’s (XLE) returns, but also the broader S&P 500 Index’s ($SPX) gains over the same periods. The momentum has been particularly strong recently, with PBA hitting its 52-week high of $42.76 in today’s trading session.

Pembina's Impressive Dividend Yield

On Sept. 27, Pembina Pipeline paid its shareholders a quarterly dividend of C$0.69 per share (approximately $0.5023 per share). Its annualized dividend of $2.01 per share translates to a 4.71% dividend yield, easily surpassing not just XLE’s 3.28% yield but the S&P 500 SPDR’s (SPY) yield of 1.23%.

PBA is currently trading at 17.67 times forward earnings, a notch below its U.S. peer Enbridge Inc.’s (ENB) 19.48x. For income-focused investors, it offers a winning combination - reliable dividends and solid growth potential. With its favorable pricing and strong dividend policy, PBA stands out in the midstream energy sector.

Pembina Pipeline Climbs After Q2 Earnings

After Pembina Pipeline reported its Q2 earnings result on Aug. 8, its stock continued to soar. With net revenue hitting C$1.22 billion - up 35% year over year - and adjusted EBITDA climbing 32.6% to C$1.09 billion, the results arrived roughly in line with Wall Street’s expectations. Higher volumes across its Pipelines, Marketing & New Ventures, and Facilities units fueled the top-line growth, while earnings per share (EPS) jumped 25% annually to C$0.75.

In Q2, Pembina closed a $3.1 billion acquisition of additional interests in Alliance and Aux Sable on April 1. Following that, it secured full ownership of Aux Sable’s U.S. operations.

The company also got a green light for the $4 billion Cedar LNG Project, partnered with the Haisla Nation. Additionally, Pembina Gas Infrastructure inked a $420 million deal with Whitecap Resources for a 50% stake in the Kaybob Complex. The Phase VIII Peace Pipeline Expansion also launched on time and under budget, marking a major milestone in meeting rising demand.

In Q2, Pembina Pipeline’s volumes soared 11% year over year to 2,716 mboe/d. This growth stemmed from a larger stake in Alliance, the reactivation of the Nipisi Pipeline, and higher volumes on the Peace Pipeline. Its Facilities arm also thrived, jumping 14% annually to 855 mboe/d, fueled by Aux Sable’s contributions and recovery from prior outages.

In Marketing & New Ventures, crude oil (CLX24) sales held steady at 100 mboe/d, while NGL sales skyrocketed by 34% to 219 mboe/d, thanks to rising demand for ethane, propane, and butane.

Moreover, the company reported a record quarterly adjusted cash flow from operating activities of C$837 million, or C$1.44 per share.

Pembina has raised its adjusted EBITDA guidance to a promising $4.20 billion to $4.35 billion range, surpassing the prior range of $4.05 billion to $4.30 billion. With a revamped 2024 capital investment program of $1.3 billion, including $0.3 billion for equity investees, the future looks bright for this energy leader.

Analysts tracking Pembina project the company’s profit to reach $2.42 per share in fiscal 2024, up 10% year over year, and grow to $2.45 in fiscal 2025.

What Do Analysts Expect for Pembina Stock?

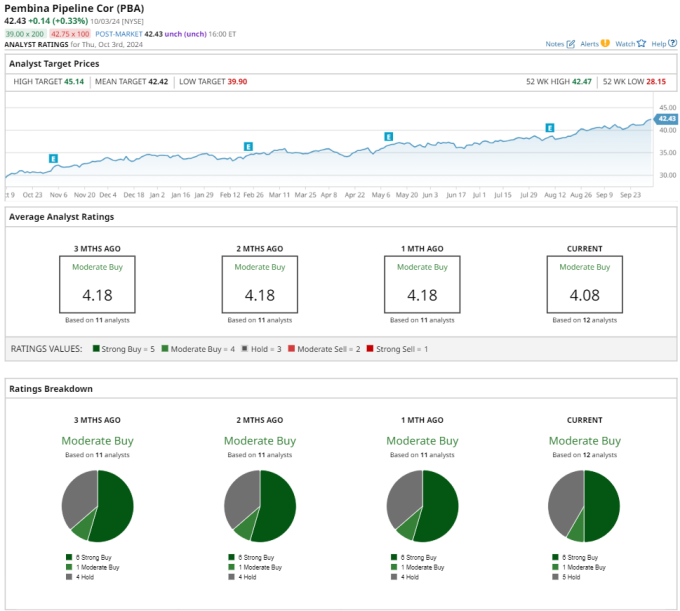

Earlier this week, Jefferies analyst Anthony Linton boosted Pembina Pipeline's price target to C$61 from C$58, while maintaining a “Buy” rating.

Linton favors Pembina over its U.S. counterpart, Enbridge, for its strong visibility on fee-based cash flow growth, solid project backlogs, and a well-structured balance sheet, which give the midstream energy operator flexibility in capital allocation.

Analysts are bullish overall on the stock’s prospects. PBA stock has a consensus “Moderate Buy” rating from 12 analysts, as six suggest a “Strong Buy,” one recommends a “Moderate Buy,” and five maintain a “Hold” rating.

Although PBA trades roughly flat with the mean price target of $42.42, the Street-high estimate of $45.15 indicates a premium of 5.8%.

More Stock Market News from

- Can This 'Strong Buy' Semiconductor Stock Top $1,000?

- Stocks Settle Higher as Strength in US Payrolls Signals Economic Resilience

- Interpublic Group's Quarterly Earnings Preview: What You Need to Know

- 2 U.S. Stocks to Bet on China Like David Tepper

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Disclosure Policy here.

Disclaimer: The copyright of this article belongs to the original author. Reposting this article is solely for the purpose of information dissemination and does not constitute any investment advice. If there is any infringement, please contact us immediately. We will make corrections or deletions as necessary. Thank you.