Howdy market watchers!

Labor Day is behind us and football season is well underway, but temperatures continue to remain stubbornly hot. In fact, much of the country has chances for warmer than usual temps in the 30-, 60- and 90-day NOAA forecasts with limited chances of increased precipitation.

Hurricane Francine has landed in the Gulf and bringing ample, isolated rain to the Southeastern states and popped energy markets after the recent selloff over concerns of disruptions to refineries. Upgraded to a Category 2 just before making landfall, the storm has nearly 40% of oil and half of natural gas production in Gulf of Mexico offline as a State of Emergency is declared in Louisiana.

This could also help the cotton market to come back to life after the recent chop below 71 cents on the December ICE contract. This soft commodity supply is relatively tight with the US crop conditions further downgraded this past week to 40 percent Good-to-Excellent from 44 percent the week prior.

However, the headwind, as for many commodities, continues to be concern over demand especially from China. Data just released for August shows weaker consumer demand, deflationary pressures and a slowing in factory activity. China’s industrial production increased by 4.5 percent in August compared to last year, but came in lower than July’s 5.1 percent figure. Retail sales only increased 2.1 percent year-over-year, down from 2.7 percent the previous month. Consumer prices increased 0.6 percent in August, higher than expected with the stated reason of food prices due to extreme weather. However, the core CPI, which excludes volatile food and energy prices, increased by only 0.3 percent last month, which was the slowest pace in over three years.

The world is watching if Beijing will begin to stimulate the economy more broadly, which should result in notable support to global commodity prices. China is expected to reduce rates by 50 basis points on some $5 trillion worth of mortgages sometime soon that will provide some relief to consumers.

Demand concerns are not only isolated to China with Europe’s Central Bank cutting deposit rates by 25 basis points this week amid slowing growth and softening inflation. All of this is leading up to the Federal Reserve’s next FOMC interest rate decision that will be announced Wednesday at 1 PM CDT. While expectations have toggled between a 25-basis point cut versus a 50 basis point cut given a softer, but relatively stable jobs market on lower unemployment, the decision is far from certain. Therefore, it has potential to be a volatile week in markets.

The US dollar continues to struggle with this week’s double top and failing to make a new high putting sellers back in charge. In fact, Friday saw the IDX gap lower and I suspect we will make new lows this week below the August 27th low at 100.400 that will likely break par. This continues to be welcome news for commodities from grains to cattle to metals.

Gold and silver performed fantastically this week with gold making new highs and silver closing above $30 per troy ounce. These metals markets will be some to watch if market uncertainty ticks higher in the coming months.

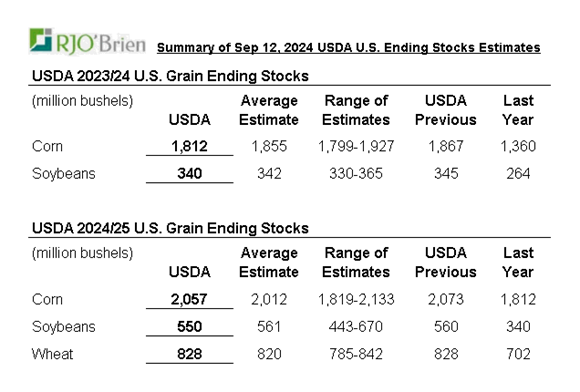

The USDA released its September WASDE and Crop Production reports on Thursday. The biggest surprise was yet another increase in average US corn yields from 183.1 bushels per acre (bpa) to 183.6 bpa versus trade guesses for a slight cut to 182.5 bpa. Harvested acres were unchanged from last month despite a cut expected that increased production forecasts to 15.186 billion bushels, 102 million bushels above trade estimates.

US soybean yields were unchanged at 53.2 bpa despite expectations for an increase to 53.3 bpa. Harvested acres were again unchanged while a cut was expected, which brought total production to 4.586 billion bushels, slightly below expectations.

New crop ending stocks were cut for corn, but not as much as thought, while soybean ending stocks were also cut despite a slight increased expected. Wheat ending stocks were unchanged though a cut was expected. World ending stocks were lower for corn, but higher for soybeans and wheat while traders were looking for a cut in global wheat ending stocks.

All in all, the report showed plenty of supplies amid a backdrop of potentially slower global economic growth. And yet, wheat, corn and soybeans all had pretty solid, bullish performance this week.

As news of the Egyptian wheat tender continue to be opaque, a private sale was reported this week with Russia being the winner. With the Russian wheat harvest progressing, we’re beginning to hear more about the impact of earlier drought and heat on final yields. Additional “States of Emergency” have been reported in several Russian regions with crops coming in lower than expected and export prices are increasing.

There is also concern developing or next year’s wheat crop that will be planted in the coming months just as in the US due to persistent drought concerns that are also true for wheat producers in the Southern US Plains. Some areas of Russia have already started planting wheat and it is reported to be the slowest planting pace since 2013.

This has sparked more fund short covering in wheat futures with the rally returning this week after last week’s profit taking as has rising tensions in the Black Sea with a Ukrainian grain vessel hit by a Russian missile last Thursday. Ukraine has also stated that wheat exports will be limited to levels below last year.

As I have advised clients, as long as we continue making new daily highs, there is likely more upside potential. Thursday’s price action was concerning as after making a new recent high, markets sold off, closing only slightly positive on report day. However, they came screaming back Friday to make a new high, then selling off mid-session, but returning near the highs and closing above Thursday’s close. Given this, I believe there is still more upside in the wheat market. In fact, I foresee $6.20 on the Dec Chicago contract and $6.30 on the Dec KC contract or just a couple cents shy of those targets.

If you’re looking to sell physical wheat, these may be targets to consider putting in place. As I continue to preach, if you sell your physical wheat, buy a call option and stay in this market. There are a number of things aligning that could see an even more meaningful pop in wheat. However, if it starts raining, beware as we could see attitudes change in a hurry.

China has continued to make purchases of US soybeans with August being a new record. As the US political landscape continues to heat up with some 50 days left until US election day, China is also starting to tilt the tables with trade disputes where it can. The anti-dumping probe on Canadian canola launched by China this past week dealt a major blow to canola market prices and added downward pressure on soybean oil. This move was seen as retaliation for Canada blocking the import of Chinese electric vehicles.

While that in itself is bilateral, I believe it is more geared as a warning to the United States to refrain from such tariffs or see such reaction placed on key US exports as candidates make pronouncements of tariffs as we heard in this last week’s debate. These headliners have so far been ignored by agriculture markets, but could become a headwind if the focus turns to restrictions on US goods.

The cattle markets have also stagged a decent recovery despite choppy macro conditions. The higher chart gaps on feeder contracts that were created at the beginning of September were filled at the end of this week. While we may see some early week strength, I would be cautious here as the Wednesday rate decision could bring about market choppiness that is not friendly to the livestock complex.

It is that time of year when we see some seasonal softness in the feeder markets and so this may be a good area to consider extending downside protection with futures, options or LRP or a combination of these tools. Fed cash cattle traded to a high of $182 in Nebraska at the end of this week. Don’t get me wrong, I believe there is more upside in the cattle market, but I feel that may come early in the new year after key elections and easing monetary policy are behind us and beginning to normalize.

Sidwell Strategies offers both CME futures and options and Livestock Risk Protection (LRP) in one place and so join the Sidwell Team today! Sidwell Strategies is the one-stop shop to protect cattle with futures, puts, LRP or a combination of all, which is probably the best strategy overall.

If you’re ready to trade commodity markets, give me a call at (580) 232-2272 or stop by my office to get your account set up and discuss risk management and marketing solutions to pursue your objectives. Self-trading accounts are also available. It is never too late to start and there is no operation too small to get a risk management and marketing plan in place.

Wishing everyone a successful trading week! Let us know if you'd like to join our daily market price and commentary text messages to stay informed!

Brady Sidwell is a Series 3 Licensed Commodity Futures Broker and Principal of Sidwell Strategies. He can be reached at (580) 232-2272 or at brady@sidwellstrategies.com. Futures and Options trading involves the risk of loss and may not be suitable for all investors. Review full disclaimer at http://www.sidwellstrategies.com/disclaimer.

On the date of publication, Brady Sidwell did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Disclosure Policy here.

Disclaimer: The copyright of this article belongs to the original author. Reposting this article is solely for the purpose of information dissemination and does not constitute any investment advice. If there is any infringement, please contact us immediately. We will make corrections or deletions as necessary. Thank you.