The Williams Companies, Inc. (WMB), headquartered in Tulsa, Oklahoma, is an energy infrastructure company that explores, produces, transports, sells, and processes natural gas and petroleum products. Valued at $50.26 billion by market cap, the company’s core operations include finding, producing, gathering, processing, and transporting natural gas and natural gas liquids. WMB owns and operates a 33,000-mile pipeline.

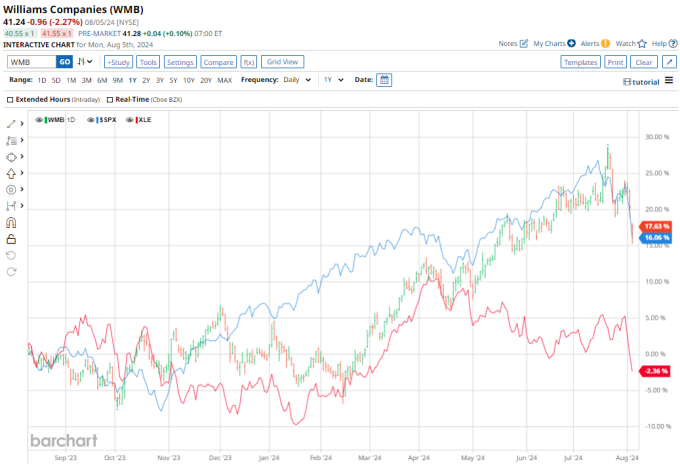

Shares of this leading midstream energy company outperformed the broader market considerably over the past year. WMB has gained 20% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 15.8%. In 2024, WMB stock is up 18.4%, surpassing SPX’s 8.7% rise on a YTD basis.

Zooming in further, WMB’s outperformance looks more pronounced compared to the S&P 500 Energy Sector SPDR (XLE). The exchange-traded fund has declined marginally over the past year. Moreover, WMB’s gains on a YTD basis outshine the ETF’s 3.1% returns over the same time frame.

On Aug. 5, WMB shares fell more than 2% after the company reported its Q2 results. Its adjusted EPS was $0.43, beating the consensus estimates of $0.39. The company reported revenue declined 5.9% year over year to $2.34 billion. For the full-year 2024, WMB expects EPS between $1.65 and $1.86 and adjusted EBITDA at the top half of its 2024 guidance range of $6.8 billion and $7.1 billion. Moreover, it expects growth capex between $1.45 billion and $1.75 billion and maintenance capex between $1.1 billion and $1.3 billion.

For the current fiscal year, ending in December, analysts expect WMB to report an EPS decline of 3.1% to $1.85 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

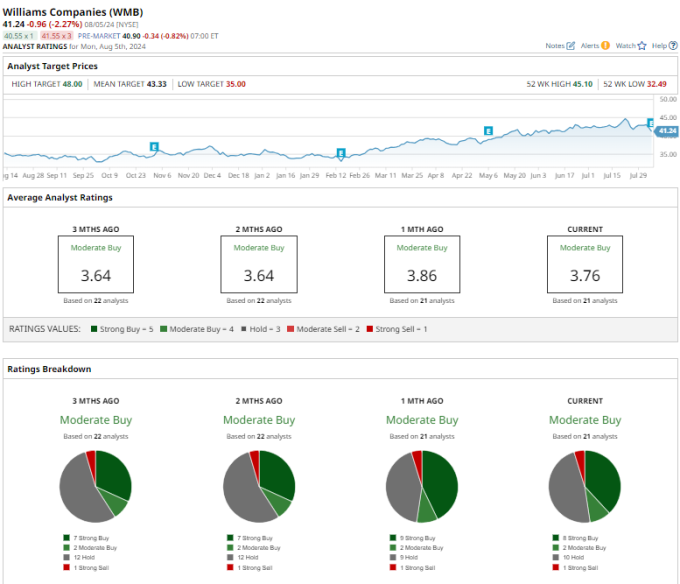

Among the 21 analysts covering WMB stock, the consensus rating is a “Moderate Buy.” That’s based on eight “Strong Buy” ratings, two “Moderate Buys,” 10 “Holds,” and one “Strong Sell.”

This configuration is slightly more bullish than three months ago, with seven suggesting a “Strong Buy.”

Recently, Barclays maintained its “Equal-Weight” rating on WMB stock and raised its target price from $38 to $41, implying a marginal potential downside from current levels.

The mean price target of $43.33 represents a 5.1% upside from WMB’s current price levels. However, the Street-high price target of $48 suggests an upside potential of 16.4%.

More Stock Market News from

- Nvidia Sinks on AI Chip Delay, But is the Stock a Sell?

- Top 100 Stocks to Buy: Is It Too Late to Buy Hamilton Beach Brands Stock?

- Intel Stock: Buy, Sell, or Steer Clear?

- Why This Sell-Rated AI Stock Just Scored an Upgrade

On the date of publication, Dipanjan Banchur did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Disclosure Policy here.

Disclaimer: The copyright of this article belongs to the original author. Reposting this article is solely for the purpose of information dissemination and does not constitute any investment advice. If there is any infringement, please contact us immediately. We will make corrections or deletions as necessary. Thank you.