Chipotle Mexican Grill (CMG), the fast-casual restaurant chain specializing in Mexican-inspired cuisine, recently posted a strong set of numbers for the second quarter. This, combined with the completion of its mammoth 50-for-1 stock split last month, has raised quite a bit of investor interest around the company.

However, with the restaurant chain also warning of margin pressure, and sitting out Friday's broad-based rally, is it too early to buy the dip in Chipotle stock? Let's take a closer look.

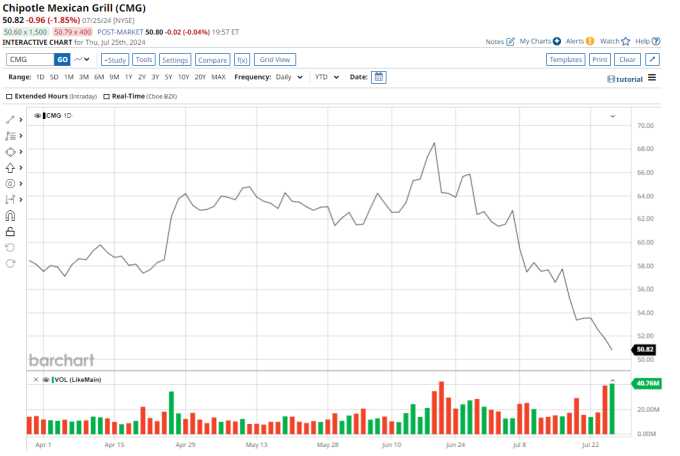

About Chipotle Mexican Grill Stock

Founded in 1993 and based out of California, Chipotle Mexican Grill (CMG) is known for its emphasis on fresh, high-quality ingredients, including naturally raised meats and organic produce. Chipotle's menu features customizable burritos, bowls, tacos, and salads, allowing customers to create their meals. Chipotle's credibility can be gauged from the fact that it is one of the most highly valued fast-casual restaurant chains in the world, with a market cap of about $70 billion.

CMG stock is up 19.3% over the past 52 weeks, and has gained 8.9% on a YTD basis.

Delicious Q2 Results from CMG

Chipotle reported better-than-expected results for Q2 of FY2024, as both revenue and earnings increased from the previous year and surpassed Street expectations. However, the chain's comments about upcoming margin pressures gave investors something to chew on.

Total revenues for the quarter came in at $2.97 billion, rising 18.3% as comparable restaurant sales increased by 11.1% from the prior year. EPS improved by 34.4% over the same period to $0.34, edging past the consensus estimate. Notably, Chipotle's EPS has consistently topped Wall Street's estimates over the past five quarters.

Cash flow generation at CMG has been robust so far in 2024, with the company reporting net cash from operating activities of $1.1 billion through June 30. The restaurant chain exited the quarter with a cash balance of $806.5 million, up from $560.6 million at the beginning of the year, while long-term debt levels increased to $4 billion from $3.8 billion at the start of the year.

Operating margin expanded to 19.7% from 17.2% while restaurant-level operating margin rose to 28.9% from 27.5% in the previous year. Looking ahead, management warned that it expects margins to come under pressure due to rising costs, which it expects to persist for the next several quarters.

"Most, if not all of this pressure is seasonal, temporary, or it's an investment that we can offset through efficiencies, and we believe our industry-leading margin structure is still intact," noted outgoing CFO Jack Hartun.

Is CMG Stock Overvalued?

Also during Q2, the company expanded its footprint with 52 company-owned restaurants opened, compared to 47 in the year-ago period. Overall, company-operated restaurants at the end of the quarter stood at 3,530, up from 3,268 in the prior year.

Looking back over the past 10 years, Chipotle's revenues and EPS have expanded at CAGRs of 11.39% and 14.75%, respectively.

Considering the company's strong position and solid fundamentals, analysts are expecting CMG to report revenue and earnings growth well above the sector median in the coming year. Forward revenue growth of 14.3% significantly outpaces the 3.73% median, while forward EPS growth at 27.93% compares to a 6.18% median.

While valid questions have been raised about CMG's valuation, the stock's growth outlook is certainly more robust than the average consumer discretionary brand. Its forward price/earnings-to-growth (PEG) ratio of 2.11 may still look a little rich, but it's actually a discount to Chipotle's five-year average valuation of 2.89 on this basis.

Sound Strategic Initiatives

Chipotle's commitment to using high-quality, ethically sourced ingredients resonates with a broad customer base, supporting brand loyalty and customer retention. Moreover, the company's strategic initiatives, such as expanding its menu with new and seasonal items, have also attracted a diverse range of customers.

Further, the company has successfully leveraged digital innovation to drive sales, with its online and app-based orders generating significant growth. Another testament to its innovative streak was evident in this quarter, as out of the 52 company-owned restaurants opened, 46 included a “Chipotlane” - the company's innovative drive-thru lane.

With a Chipotlane, customers can place their orders in advance through the Chipotle app or at a digital kiosk, and then pick up their food without leaving their cars. Chipotlane has been a hit, as the former chief development officer of the company remarked in 2023 that it has resulted in 10% to 15% higher average sales at restaurants with lanes than at restaurants without lanes.

With plans to double its locations in North America, its entry into the Middle East last year, and a new leadership team focused on international growth, particularly in Europe, Chipotle's expansion spree is not showing any signs of slowing down.

Analysts See More Upside for CMG

Analysts have a consensus rating of “Moderate Buy” for CMG stock, with a mean target price of $65.55. This suggests an expected upside potential of about 31.5% from Friday's close.

Out of 29 analysts covering the stock, 19 have a “Strong Buy” rating, 1 has a “Moderate Buy” rating, and 9 have a “Hold” rating.

On the date of publication, Pathikrit Bose did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Disclosure Policy here.

Disclaimer: The copyright of this article belongs to the original author. Reposting this article is solely for the purpose of information dissemination and does not constitute any investment advice. If there is any infringement, please contact us immediately. We will make corrections or deletions as necessary. Thank you.